Market Prediction Tutorial

MarketFlow Running Time: Approximately 6 minutes

Machine learning subsumes technical analysis because collectively, technical analysis is just a set of features for market prediction. We can use machine learning as a feature blender for moving averages, indicators such as RSI and ADX, and even representations of chart formations such as double tops and head-and-shoulder patterns.

We are not directly predicting net return in our models, although that is the ultimate goal. By characterizing the market with models, we can increase the Return On Investment (ROI). We have a wide range of dependent or target variables from which to choose, not just net return. There is more power in building a classifier rather than a more traditional regression model, so we want to define binary conditions such as whether or not today is going to be a trend day, rather than a numerical prediction of today’s return.

In this tutorial, we will train a model that predicts whether or not the next day will have a larger-than-average range. This is important for deciding which system to deploy on the prediction day. If our model gives us predictive power, then we can filter out those days where trading a given system is a losing strategy.

Step 1: From the examples directory, change your

directory:

cd "Trading Model"

Before running MarketFlow, let’s briefly review the configuration

files in the config directory:

market.yml:The MarketFlow configuration file

model.yml:The AlphaPy configuration file

In market.yml, we limit our model to six stocks in the target

group test, going back 2000 trading days. You can define any

group of stock symbols in the groups section, and then set

the target_group attribute in the market section to the

name of that group.

This is a 1-day forecast, but we also use those features that can

be calculated at the market open, such as gap information in the

leaders section. In the features section, we define many

variables for moving averages, historical range, RSI, volatility,

and volume.

market:

create_model : True

data_fractal : 1d

data_history : 500

forecast_period : 1

fractal : 1d

lag_period : 1

leaders : ['gap', 'gapbadown', 'gapbaup', 'gapdown', 'gapup']

predict_history : 100

schema : yahoo

subject : stock

target_group : test

groups:

all : ['aaoi', 'aapl', 'acia', 'adbe', 'adi', 'adp', 'agn', 'aig', 'akam',

'algn', 'alk', 'alxn', 'amat', 'amba', 'amd', 'amgn', 'amt', 'amzn',

'antm', 'arch', 'asml', 'athn', 'atvi', 'auph', 'avgo', 'axp', 'ayx',

'azo', 'ba', 'baba', 'bac', 'bby', 'bidu', 'biib', 'brcd', 'bvsn',

'bwld', 'c', 'cacc', 'cara', 'casy', 'cat', 'cde', 'celg', 'cern',

'chkp', 'chtr', 'clvs', 'cme', 'cmg', 'cof', 'cohr', 'comm', 'cost',

'cpk', 'crm', 'crus', 'csco', 'ctsh', 'ctxs', 'csx', 'cvs', 'cybr',

'data', 'ddd', 'deck', 'dgaz', 'dia', 'dis', 'dish', 'dnkn', 'dpz',

'drys', 'dust', 'ea', 'ebay', 'edc', 'edz', 'eem', 'elli', 'eog',

'esrx', 'etrm', 'ewh', 'ewt', 'expe', 'fang', 'fas', 'faz', 'fb',

'fcx', 'fdx', 'ffiv', 'fit', 'five', 'fnsr', 'fslr', 'ftnt', 'gddy',

'gdx', 'gdxj', 'ge', 'gild', 'gld', 'glw', 'gm', 'googl', 'gpro',

'grub', 'gs', 'gwph', 'hal', 'has', 'hd', 'hdp', 'hlf', 'hog', 'hum',

'ibb', 'ibm', 'ice', 'idxx', 'ilmn', 'ilmn', 'incy', 'intc', 'intu',

'ip', 'isrg', 'iwm', 'ivv', 'iwf', 'iwm', 'jack', 'jcp', 'jdst', 'jnj',

'jnpr', 'jnug', 'jpm', 'kite', 'klac', 'ko', 'kss', 'labd', 'labu',

'len', 'lite', 'lmt', 'lnkd', 'lrcx', 'lulu', 'lvs', 'mbly', 'mcd',

'mchp', 'mdy', 'meoh', 'mnst', 'mo', 'momo', 'mon', 'mrk', 'ms', 'msft',

'mtb', 'mu', 'nflx', 'nfx', 'nke', 'ntap', 'ntes', 'ntnx', 'nugt',

'nvda', 'nxpi', 'nxst', 'oii', 'oled', 'orcl', 'orly', 'p', 'panw',

'pcln', 'pg', 'pm', 'pnra', 'prgo', 'pxd', 'pypl', 'qcom', 'qqq',

'qrvo', 'rht', 'sam', 'sbux', 'sds', 'sgen', 'shld', 'shop', 'sig',

'sina', 'siri', 'skx', 'slb', 'slv', 'smh', 'snap', 'sncr', 'soda',

'splk', 'spy', 'stld', 'stmp', 'stx', 'svxy', 'swks', 'symc', 't',

'tbt', 'teva', 'tgt', 'tho', 'tlt', 'tmo', 'tna', 'tqqq', 'trip',

'tsla', 'ttwo', 'tvix', 'twlo', 'twtr', 'tza', 'uaa', 'ugaz', 'uhs',

'ulta', 'ulti', 'unh', 'unp', 'upro', 'uri', 'ups', 'uri', 'uthr',

'utx', 'uvxy', 'v', 'veev', 'viav', 'vlo', 'vmc', 'vrsn', 'vrtx', 'vrx',

'vwo', 'vxx', 'vz', 'wday', 'wdc', 'wfc', 'wfm', 'wmt', 'wynn', 'x',

'xbi', 'xhb', 'xiv', 'xle', 'xlf', 'xlk', 'xlnx', 'xom', 'xlp', 'xlu',

'xlv', 'xme', 'xom', 'wix', 'yelp', 'z']

etf : ['dia', 'dust', 'edc', 'edz', 'eem', 'ewh', 'ewt', 'fas', 'faz',

'gld', 'hyg', 'iwm', 'ivv', 'iwf', 'jnk', 'mdy', 'nugt', 'qqq',

'sds', 'smh', 'spy', 'tbt', 'tlt', 'tna', 'tvix', 'tza', 'upro',

'uvxy', 'vwo', 'vxx', 'xhb', 'xiv', 'xle', 'xlf', 'xlk', 'xlp',

'xlu', 'xlv', 'xme']

tech : ['aapl', 'adbe', 'amat', 'amgn', 'amzn', 'avgo', 'baba', 'bidu',

'brcd', 'csco', 'ddd', 'emc', 'expe', 'fb', 'fit', 'fslr', 'goog',

'intc', 'isrg', 'lnkd', 'msft', 'nflx', 'nvda', 'pcln', 'qcom',

'qqq', 'tsla', 'twtr']

test : ['aapl', 'amzn', 'goog', 'fb', 'nvda', 'tsla']

features: ['abovema_3', 'abovema_5', 'abovema_10', 'abovema_20', 'abovema_50',

'adx', 'atr', 'bigdown', 'bigup', 'diminus', 'diplus', 'doji',

'gap', 'gapbadown', 'gapbaup', 'gapdown', 'gapup',

'hc', 'hh', 'ho', 'hl', 'lc', 'lh', 'll', 'lo', 'hookdown', 'hookup',

'inside', 'outside', 'madelta_3', 'madelta_5', 'madelta_7', 'madelta_10',

'madelta_12', 'madelta_15', 'madelta_18', 'madelta_20', 'madelta',

'net', 'netdown', 'netup', 'nr_3', 'nr_4', 'nr_5', 'nr_7', 'nr_8',

'nr_10', 'nr_18', 'roi', 'roi_2', 'roi_3', 'roi_4', 'roi_5', 'roi_10',

'roi_20', 'rr_1_4', 'rr_1_7', 'rr_1_10', 'rr_2_5', 'rr_2_7', 'rr_2_10',

'rr_3_8', 'rr_3_14', 'rr_4_10', 'rr_4_20', 'rr_5_10', 'rr_5_20',

'rr_5_30', 'rr_6_14', 'rr_6_25', 'rr_7_14', 'rr_7_35', 'rr_8_22',

'rrhigh', 'rrlow', 'rrover', 'rrunder', 'rsi_3', 'rsi_4', 'rsi_5',

'rsi_6', 'rsi_8', 'rsi_10', 'rsi_14', 'sep_3_3', 'sep_5_5', 'sep_8_8',

'sep_10_10', 'sep_14_14', 'sep_21_21', 'sep_30_30', 'sep_40_40',

'sephigh', 'seplow', 'trend', 'vma', 'vmover', 'vmratio', 'vmunder',

'volatility_3', 'volatility_5', 'volatility', 'volatility_20',

'wr_2', 'wr_3', 'wr', 'wr_5', 'wr_6', 'wr_7', 'wr_10']

aliases:

atr : 'ma_truerange'

aver : 'ma_hlrange'

cma : 'ma_close'

cmax : 'highest_close'

cmin : 'lowest_close'

hc : 'higher_close'

hh : 'higher_high'

hl : 'higher_low'

ho : 'higher_open'

hmax : 'highest_high'

hmin : 'lowest_high'

lc : 'lower_close'

lh : 'lower_high'

ll : 'lower_low'

lo : 'lower_open'

lmax : 'highest_low'

lmin : 'lowest_low'

net : 'net_close'

netdown : 'down_net'

netup : 'up_net'

omax : 'highest_open'

omin : 'lowest_open'

rmax : 'highest_hlrange'

rmin : 'lowest_hlrange'

rr : 'maratio_hlrange'

rixc : 'rindex_close_high_low'

rixo : 'rindex_open_high_low'

roi : 'netreturn_close'

rsi : 'rsi_close'

sepma : 'ma_sep'

vma : 'ma_volume'

vmratio : 'maratio_volume'

upmove : 'net_high'

variables:

abovema : 'close > cma_50'

belowma : 'close < cma_50'

bigup : 'rrover & sephigh & netup'

bigdown : 'rrover & sephigh & netdown'

doji : 'sepdoji & rrunder'

hookdown : 'open > high[1] & close < close[1]'

hookup : 'open < low[1] & close > close[1]'

inside : 'low > low[1] & high < high[1]'

madelta : '(close - cma_50) / atr_10'

nr : 'hlrange == rmin_4'

outside : 'low < low[1] & high > high[1]'

roihigh : 'roi_5 >= 5'

roilow : 'roi_5 < -5'

roiminus : 'roi_5 < 0'

roiplus : 'roi_5 > 0'

rrhigh : 'rr_1_10 >= 1.2'

rrlow : 'rr_1_10 <= 0.8'

rrover : 'rr_1_10 >= 1.0'

rrunder : 'rr_1_10 < 1.0'

sep : 'rixc_1 - rixo_1'

sepdoji : 'abs(sep) <= 15'

sephigh : 'abs(sep_1_1) >= 70'

seplow : 'abs(sep_1_1) <= 30'

trend : 'rrover & sephigh'

vmover : 'vmratio >= 1'

vmunder : 'vmratio < 1'

volatility : 'atr_10 / close'

wr : 'hlrange == rmax_4'

In each of the tutorials, we experiment with different options in

model.yml to run AlphaPy. Here, we first apply univariate feature

selection and then run a random forest classifier with Recursive

Feature Elimination, including Cross-Validation (RFECV). When you

choose RFECV, the process takes much longer, so if you want to see

more logging, then increase the verbosity level in the pipeline

section.

Since stock prices are time series data, we apply the runs_test

function to twelve features in the treatments section. Treatments

are powerful because you can write any function to extrapolate new

features from existing ones. AlphaPy provides some of these functions

in the alphapy.features module, but it can also import external

functions as well.

Our target variable is rrover, the ratio of the 1-day range to

the 10-day average high/low range. If that ratio is greater than

or equal to 1.0, then the value of rrover is True. This is

what we are trying to predict.

project:

directory : .

file_extension : csv

submission_file :

submit_probas : False

data:

drop : ['date', 'tag', 'open', 'high', 'low', 'close', 'volume', 'adjclose',

'low[1]', 'high[1]', 'net', 'close[1]', 'rmin_3', 'rmin_4', 'rmin_5',

'rmin_7', 'rmin_8', 'rmin_10', 'rmin_18', 'pval', 'mval', 'vma',

'rmax_2', 'rmax_3', 'rmax_4', 'rmax_5', 'rmax_6', 'rmax_7', 'rmax_10']

features : '*'

sampling :

option : True

method : under_random

ratio : 0.5

sentinel : -1

separator : ','

shuffle : True

split : 0.4

target : rrover

target_value : True

model:

algorithms : ['RF']

balance_classes : True

calibration :

option : False

type : isotonic

cv_folds : 3

estimators : 501

feature_selection :

option : True

percentage : 50

uni_grid : [5, 10, 15, 20, 25]

score_func : f_classif

grid_search :

option : False

iterations : 100

random : True

subsample : True

sampling_pct : 0.25

pvalue_level : 0.01

rfe :

option : True

step : 10

scoring_function : 'roc_auc'

type : classification

features:

clustering :

option : False

increment : 3

maximum : 30

minimum : 3

counts :

option : False

encoding :

rounding : 3

type : factorize

factors : []

interactions :

option : True

poly_degree : 2

sampling_pct : 5

isomap :

option : False

components : 2

neighbors : 5

logtransform :

option : False

numpy :

option : False

pca :

option : False

increment : 3

maximum : 15

minimum : 3

whiten : False

scaling :

option : True

type : standard

scipy :

option : False

text :

ngrams : 1

vectorize : False

tsne :

option : False

components : 2

learning_rate : 1000.0

perplexity : 30.0

variance :

option : True

threshold : 0.1

treatments:

doji : ['alphapy.features', 'runs_test', ['all'], 18]

hc : ['alphapy.features', 'runs_test', ['all'], 18]

hh : ['alphapy.features', 'runs_test', ['all'], 18]

hl : ['alphapy.features', 'runs_test', ['all'], 18]

ho : ['alphapy.features', 'runs_test', ['all'], 18]

rrhigh : ['alphapy.features', 'runs_test', ['all'], 18]

rrlow : ['alphapy.features', 'runs_test', ['all'], 18]

rrover : ['alphapy.features', 'runs_test', ['all'], 18]

rrunder : ['alphapy.features', 'runs_test', ['all'], 18]

sephigh : ['alphapy.features', 'runs_test', ['all'], 18]

seplow : ['alphapy.features', 'runs_test', ['all'], 18]

trend : ['alphapy.features', 'runs_test', ['all'], 18]

pipeline:

number_jobs : -1

seed : 10231

verbosity : 0

plots:

calibration : True

confusion_matrix : True

importances : True

learning_curve : True

roc_curve : True

xgboost:

stopping_rounds : 20

Step 2: Now, let’s run MarketFlow:

mflow --pdate 2017-10-01

As mflow runs, you will see the progress of the workflow,

and the logging output is saved in market_flow.log. When the

workflow completes, your project structure will look like this,

with a different datestamp:

Trading Model

├── market_flow.log

├── config

├── algos.yml

├── market.yml

├── model.yml

└── data

└── input

├── test_20170420.csv

├── test.csv

├── train_20170420.csv

├── train.csv

└── model

├── feature_map_20170420.pkl

├── model_20170420.pkl

└── output

├── predictions_20170420.csv

├── probabilities_20170420.csv

├── rankings_20170420.csv

└── plots

├── calibration_test.png

├── calibration_train.png

├── confusion_test_RF.png

├── confusion_train_RF.png

├── feature_importance_train_RF.png

├── learning_curve_train_RF.png

├── roc_curve_test.png

├── roc_curve_train.png

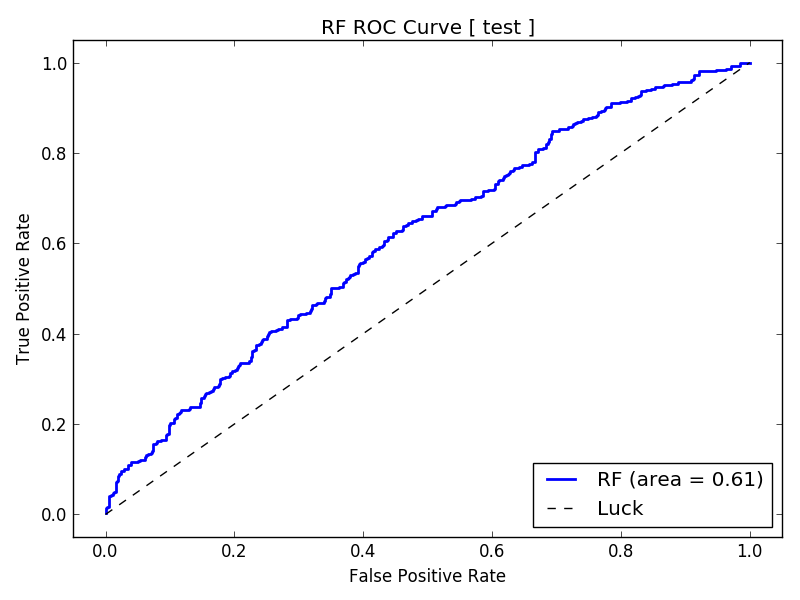

Let’s look at the results in the plots directory. Since our

scoring function was roc_auc, we examine the ROC Curve first.

The AUC is approximately 0.61, which is not very high but in the

context of the stock market, we may still be able to derive

some predictive power. Further, we are running the model on a

relatively small sample of stocks, as denoted by the jittery

line of the ROC Curve.

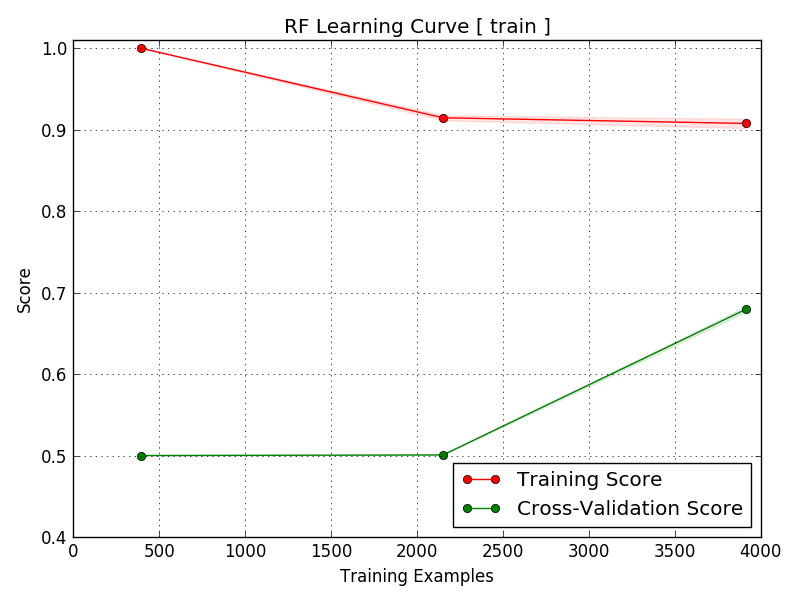

We can benefit from more samples, as the learning curve shows that the training and cross-validation lines have yet to converge.

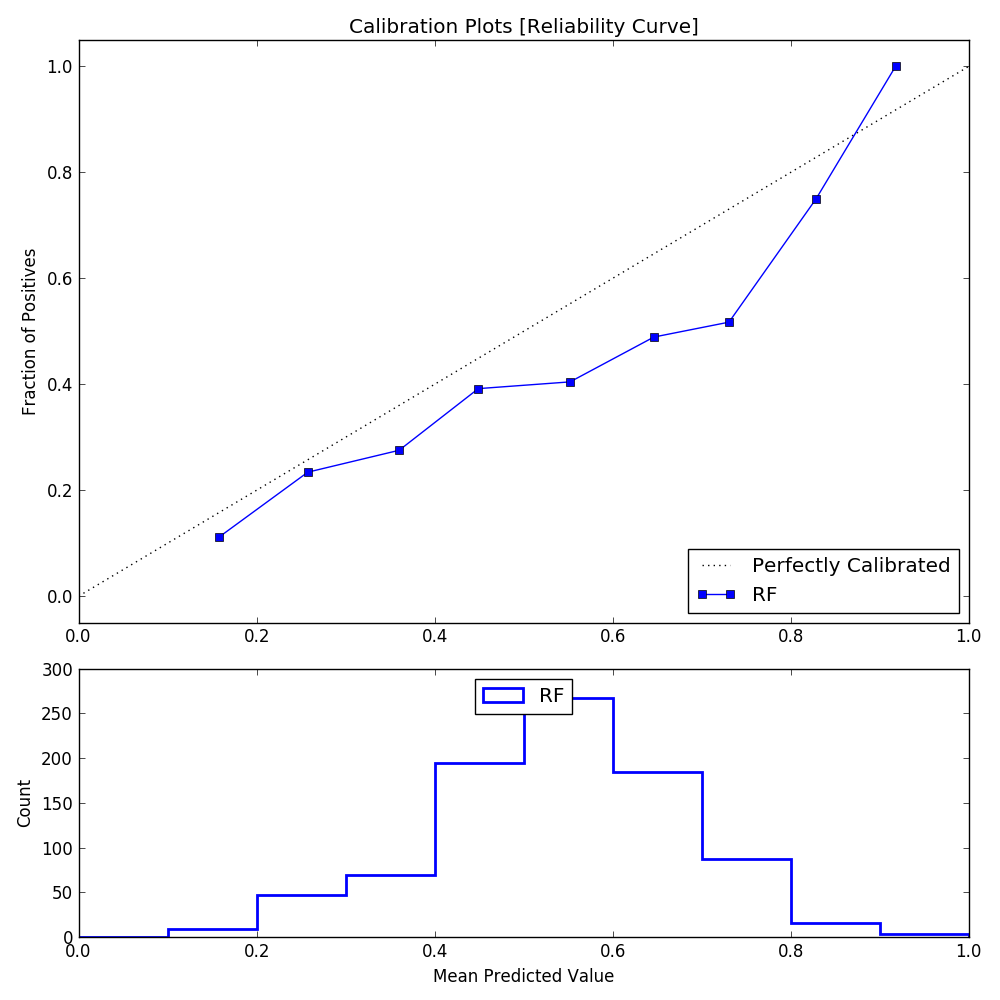

The good news is that even with a relatively small number of testing points, the Reliability Curve slopes upward from left to right, with the dotted line denoting a perfect classifier.

To get better accuracy, we can raise our threshold to find the best candidates, since they are ranked by probability, but this also means limiting our pool of stocks. Let’s take a closer look at the rankings file.

Step 3: From the command line, enter:

jupyter notebook

Step 4: Click on the notebook named:

A Trading Model.ipynb

Step 5: Run the commands in the notebook, making sure that

when you read in the rankings file, change the date to match

the result from the ls command.

Conclusion We can predict large-range days with some confidence,

but only at a higher probability threshold. This is important for

choosing the correct system on any given day. We can achieve

better results with more data, so we recommend expanding the

stock universe, e.g., a group with at least 100 members going

five years back.