MarketFlow¶

MarketFlow transforms financial market data into machine learning models for making market predictions. The platform gets stock price data from Yahoo Finance (end-of-day) and Google Finance (intraday), transforming the data into canonical form for training and testing. MarketFlow is powerful because you can easily apply new features to groups of stocks simultaneously using our Variable Definition Language (VDL). All of the dataframes are aggregated and split into training and testing files for input into AlphaPy.

Data Sources¶

MarketFlow gets daily stock prices from Yahoo Finance and intraday

stock prices from Google Finance. Both data sources have the standard

primitives: Open, High, Low, Close, and Volume.

For daily data, there is a Date timestamp and for intraday data,

there is a Datetime timestamp. We augment the intraday data with

a bar_number field to mark the end of the trading day. All trading

days do not end at 4:00 pm EST, as there are holiday trading days

that are shortened.

Date |

Open |

High |

Low |

Close |

Volume |

2017-03-01 |

853.05 |

854.83 |

849.01 |

853.08 |

2752000 |

2017-03-02 |

853.08 |

854.82 |

847.28 |

848.91 |

2129200 |

2017-03-03 |

847.20 |

851.99 |

846.27 |

849.88 |

1941100 |

2017-03-06 |

845.23 |

848.49 |

841.12 |

846.61 |

2598400 |

2017-03-07 |

845.48 |

848.46 |

843.75 |

846.02 |

2217800 |

2017-03-08 |

848.00 |

853.07 |

846.79 |

850.50 |

2286500 |

2017-03-09 |

851.00 |

856.40 |

850.31 |

853.00 |

2040600 |

2017-03-10 |

857.00 |

857.35 |

851.72 |

852.46 |

2422000 |

2017-03-13 |

851.77 |

855.69 |

851.71 |

854.59 |

1906100 |

2017-03-14 |

853.55 |

853.75 |

847.55 |

852.53 |

2128700 |

2017-03-15 |

854.33 |

854.45 |

847.11 |

852.97 |

2556700 |

2017-03-16 |

855.30 |

855.50 |

850.51 |

853.42 |

1832600 |

2017-03-17 |

853.49 |

853.83 |

850.64 |

852.31 |

3380700 |

2017-03-20 |

851.51 |

857.80 |

851.01 |

856.97 |

2223300 |

2017-03-21 |

858.84 |

862.80 |

841.31 |

843.20 |

4349100 |

2017-03-22 |

840.43 |

849.37 |

839.05 |

848.06 |

2636200 |

2017-03-23 |

848.20 |

850.89 |

844.80 |

847.38 |

1945700 |

2017-03-24 |

851.68 |

851.80 |

843.53 |

845.61 |

2118300 |

2017-03-27 |

838.07 |

850.30 |

833.50 |

846.82 |

2754200 |

2017-03-28 |

851.75 |

858.46 |

850.10 |

856.00 |

3033000 |

2017-03-29 |

859.05 |

876.44 |

859.02 |

874.32 |

4464400 |

2017-03-30 |

874.95 |

877.06 |

871.66 |

876.34 |

2745800 |

2017-03-31 |

877.00 |

890.35 |

876.65 |

886.54 |

3910700 |

Note

Normal market hours are 9:30 am to 4:00 pm EST. Here, we retrieved the data from the CST time zone, one hour ahead.

datetime |

open |

high |

low |

close |

volume |

bar_number |

end_of_day |

2017-03-31 08:30:00 |

877.00 |

877.06 |

876.66 |

877.06 |

43910 |

0 |

False |

2017-03-31 08:40:00 |

877.00 |

881.74 |

876.65 |

880.66 |

192152 |

1 |

False |

2017-03-31 08:50:00 |

881.00 |

886.01 |

880.45 |

884.67 |

249892 |

2 |

False |

2017-03-31 09:00:00 |

884.83 |

886.08 |

883.50 |

883.90 |

148034 |

3 |

False |

2017-03-31 09:10:00 |

883.90 |

886.44 |

883.84 |

885.72 |

118518 |

4 |

False |

2017-03-31 09:20:00 |

885.82 |

886.39 |

884.68 |

886.30 |

76880 |

5 |

False |

2017-03-31 09:30:00 |

886.14 |

886.74 |

885.07 |

885.73 |

74180 |

6 |

False |

2017-03-31 09:40:00 |

885.80 |

886.20 |

885.13 |

886.20 |

77154 |

7 |

False |

2017-03-31 09:50:00 |

886.21 |

887.61 |

885.77 |

887.51 |

86971 |

8 |

False |

2017-03-31 10:00:00 |

887.59 |

888.35 |

886.83 |

887.81 |

111998 |

9 |

False |

2017-03-31 10:10:00 |

887.80 |

888.72 |

887.59 |

888.60 |

64497 |

10 |

False |

2017-03-31 10:20:00 |

888.62 |

890.35 |

888.44 |

889.82 |

101562 |

11 |

False |

2017-03-31 10:30:00 |

889.81 |

889.96 |

888.83 |

889.83 |

42580 |

12 |

False |

2017-03-31 10:40:00 |

889.70 |

889.92 |

887.32 |

887.61 |

88559 |

13 |

False |

2017-03-31 10:50:00 |

887.68 |

889.58 |

887.66 |

889.01 |

45492 |

14 |

False |

2017-03-31 11:00:00 |

889.12 |

889.26 |

887.25 |

888.34 |

39841 |

15 |

False |

2017-03-31 11:10:00 |

888.52 |

889.00 |

887.66 |

887.66 |

24525 |

16 |

False |

2017-03-31 11:20:00 |

887.83 |

888.74 |

887.67 |

888.14 |

35031 |

17 |

False |

2017-03-31 11:30:00 |

888.14 |

888.87 |

888.10 |

888.87 |

24460 |

18 |

False |

2017-03-31 11:40:00 |

888.91 |

889.47 |

888.76 |

888.96 |

38921 |

19 |

False |

2017-03-31 11:50:00 |

888.87 |

889.06 |

888.47 |

888.89 |

35439 |

20 |

False |

2017-03-31 12:00:00 |

888.86 |

889.50 |

888.82 |

889.40 |

25933 |

21 |

False |

2017-03-31 12:10:00 |

889.40 |

889.94 |

889.35 |

889.86 |

35120 |

22 |

False |

2017-03-31 12:20:00 |

889.90 |

890.25 |

889.51 |

889.57 |

38429 |

23 |

False |

2017-03-31 12:30:00 |

889.70 |

889.79 |

889.20 |

889.79 |

18435 |

24 |

False |

2017-03-31 12:40:00 |

889.80 |

889.93 |

889.28 |

889.50 |

25481 |

25 |

False |

2017-03-31 12:50:00 |

889.60 |

889.99 |

889.50 |

889.77 |

26536 |

26 |

False |

2017-03-31 13:00:00 |

889.70 |

889.73 |

888.33 |

888.49 |

35556 |

27 |

False |

2017-03-31 13:10:00 |

888.31 |

888.64 |

887.80 |

888.45 |

39215 |

28 |

False |

2017-03-31 13:20:00 |

888.58 |

888.58 |

887.09 |

887.15 |

43771 |

29 |

False |

2017-03-31 13:30:00 |

887.18 |

888.40 |

887.05 |

888.13 |

36830 |

30 |

False |

2017-03-31 13:40:00 |

888.22 |

888.99 |

887.68 |

888.78 |

29510 |

31 |

False |

2017-03-31 13:50:00 |

888.79 |

888.99 |

888.35 |

888.58 |

30370 |

32 |

False |

2017-03-31 14:00:00 |

888.66 |

888.82 |

887.02 |

887.02 |

48011 |

33 |

False |

2017-03-31 14:10:00 |

887.02 |

888.30 |

886.80 |

888.15 |

41046 |

34 |

False |

2017-03-31 14:20:00 |

888.14 |

889.00 |

888.06 |

888.55 |

38660 |

35 |

False |

2017-03-31 14:30:00 |

888.58 |

888.83 |

888.30 |

888.40 |

39304 |

36 |

False |

2017-03-31 14:40:00 |

888.40 |

888.60 |

888.01 |

888.45 |

57289 |

37 |

False |

2017-03-31 14:50:00 |

888.39 |

889.32 |

888.16 |

888.17 |

105594 |

38 |

False |

2017-03-31 15:00:00 |

888.43 |

888.54 |

886.54 |

886.94 |

518134 |

39 |

True |

Note

You can get Google intraday data going back a maximum of 50 days. If you want to build your own historical record, then we recommend that you save the data on an ongoing basis for a a larger backtesting window.

Domain Configuration¶

The market configuration file (market.yml) is written in YAML

and is divided into logical sections reflecting different parts

of MarketFlow. This file is stored in the config directory

of your project, along with the model.yml and algos.yml files.

The market section has the following parameters:

data_history:Number of periods of historical data to retrieve.

forecast_period:Number of periods to forecast for the target variable.

fractal:The time quantum for the data feed, represented by an integer followed by a character code. The string “1d” is one day, and “5m” is five minutes.

leaders:A list of features that are coincident with the target variable. For example, with daily stock market data, the

Openis considered to be a leader because it is recorded at the market open. In contrast, the dailyHighorLowcannot be known until the the market close.predict_history:This is the minimum number of periods required to derive all of the features in prediction mode on a given date. If you use a rolling mean of 50 days, then the

predict_historyshould be set to at least 50 to have a valid value on the prediction date.schema:This string uniquely identifies the subject matter of the data. A schema could be

pricesfor identifying market data.target_group:The name of the group selected from the

groupssection, e.g., a set of stock symbols.

market:

data_history : 2000

forecast_period : 1

fractal : 1d

leaders : ['gap', 'gapbadown', 'gapbaup', 'gapdown', 'gapup']

predict_history : 100

schema : prices

target_group : test

groups:

all : ['aaoi', 'aapl', 'acia', 'adbe', 'adi', 'adp', 'agn', 'aig', 'akam',

'algn', 'alk', 'alxn', 'amat', 'amba', 'amd', 'amgn', 'amt', 'amzn',

'antm', 'arch', 'asml', 'athn', 'atvi', 'auph', 'avgo', 'axp', 'ayx',

'azo', 'ba', 'baba', 'bac', 'bby', 'bidu', 'biib', 'brcd', 'bvsn',

'bwld', 'c', 'cacc', 'cara', 'casy', 'cat', 'cde', 'celg', 'cern',

'chkp', 'chtr', 'clvs', 'cme', 'cmg', 'cof', 'cohr', 'comm', 'cost',

'cpk', 'crm', 'crus', 'csco', 'ctsh', 'ctxs', 'csx', 'cvs', 'cybr',

'data', 'ddd', 'deck', 'dgaz', 'dia', 'dis', 'dish', 'dnkn', 'dpz',

'drys', 'dust', 'ea', 'ebay', 'edc', 'edz', 'eem', 'elli', 'eog',

'esrx', 'etrm', 'ewh', 'ewt', 'expe', 'fang', 'fas', 'faz', 'fb',

'fcx', 'fdx', 'ffiv', 'fit', 'five', 'fnsr', 'fslr', 'ftnt', 'gddy',

'gdx', 'gdxj', 'ge', 'gild', 'gld', 'glw', 'gm', 'googl', 'gpro',

'grub', 'gs', 'gwph', 'hal', 'has', 'hd', 'hdp', 'hlf', 'hog', 'hum',

'ibb', 'ibm', 'ice', 'idxx', 'ilmn', 'ilmn', 'incy', 'intc', 'intu',

'ip', 'isrg', 'iwm', 'ivv', 'iwf', 'iwm', 'jack', 'jcp', 'jdst', 'jnj',

'jnpr', 'jnug', 'jpm', 'kite', 'klac', 'ko', 'kss', 'labd', 'labu',

'len', 'lite', 'lmt', 'lnkd', 'lrcx', 'lulu', 'lvs', 'mbly', 'mcd',

'mchp', 'mdy', 'meoh', 'mnst', 'mo', 'momo', 'mon', 'mrk', 'ms', 'msft',

'mtb', 'mu', 'nflx', 'nfx', 'nke', 'ntap', 'ntes', 'ntnx', 'nugt',

'nvda', 'nxpi', 'nxst', 'oii', 'oled', 'orcl', 'orly', 'p', 'panw',

'pcln', 'pg', 'pm', 'pnra', 'prgo', 'pxd', 'pypl', 'qcom', 'qqq',

'qrvo', 'rht', 'sam', 'sbux', 'sds', 'sgen', 'shld', 'shop', 'sig',

'sina', 'siri', 'skx', 'slb', 'slv', 'smh', 'snap', 'sncr', 'soda',

'splk', 'spy', 'stld', 'stmp', 'stx', 'svxy', 'swks', 'symc', 't',

'tbt', 'teva', 'tgt', 'tho', 'tlt', 'tmo', 'tna', 'tqqq', 'trip',

'tsla', 'ttwo', 'tvix', 'twlo', 'twtr', 'tza', 'uaa', 'ugaz', 'uhs',

'ulta', 'ulti', 'unh', 'unp', 'upro', 'uri', 'ups', 'uri', 'uthr',

'utx', 'uvxy', 'v', 'veev', 'viav', 'vlo', 'vmc', 'vrsn', 'vrtx', 'vrx',

'vwo', 'vxx', 'vz', 'wday', 'wdc', 'wfc', 'wfm', 'wmt', 'wynn', 'x',

'xbi', 'xhb', 'xiv', 'xle', 'xlf', 'xlk', 'xlnx', 'xom', 'xlp', 'xlu',

'xlv', 'xme', 'xom', 'wix', 'yelp', 'z']

etf : ['dia', 'dust', 'edc', 'edz', 'eem', 'ewh', 'ewt', 'fas', 'faz',

'gld', 'hyg', 'iwm', 'ivv', 'iwf', 'jnk', 'mdy', 'nugt', 'qqq',

'sds', 'smh', 'spy', 'tbt', 'tlt', 'tna', 'tvix', 'tza', 'upro',

'uvxy', 'vwo', 'vxx', 'xhb', 'xiv', 'xle', 'xlf', 'xlk', 'xlp',

'xlu', 'xlv', 'xme']

tech : ['aapl', 'adbe', 'amat', 'amgn', 'amzn', 'avgo', 'baba', 'bidu',

'brcd', 'csco', 'ddd', 'emc', 'expe', 'fb', 'fit', 'fslr', 'goog',

'intc', 'isrg', 'lnkd', 'msft', 'nflx', 'nvda', 'pcln', 'qcom',

'qqq', 'tsla', 'twtr']

test : ['aapl', 'amzn', 'goog', 'fb', 'nvda', 'tsla']

features: ['abovema_3', 'abovema_5', 'abovema_10', 'abovema_20', 'abovema_50',

'adx', 'atr', 'bigdown', 'bigup', 'diminus', 'diplus', 'doji',

'gap', 'gapbadown', 'gapbaup', 'gapdown', 'gapup',

'hc', 'hh', 'ho', 'hl', 'lc', 'lh', 'll', 'lo', 'hookdown', 'hookup',

'inside', 'outside', 'madelta_3', 'madelta_5', 'madelta_7', 'madelta_10',

'madelta_12', 'madelta_15', 'madelta_18', 'madelta_20', 'madelta',

'net', 'netdown', 'netup', 'nr_3', 'nr_4', 'nr_5', 'nr_7', 'nr_8',

'nr_10', 'nr_18', 'roi', 'roi_2', 'roi_3', 'roi_4', 'roi_5', 'roi_10',

'roi_20', 'rr_1_4', 'rr_1_7', 'rr_1_10', 'rr_2_5', 'rr_2_7', 'rr_2_10',

'rr_3_8', 'rr_3_14', 'rr_4_10', 'rr_4_20', 'rr_5_10', 'rr_5_20',

'rr_5_30', 'rr_6_14', 'rr_6_25', 'rr_7_14', 'rr_7_35', 'rr_8_22',

'rrhigh', 'rrlow', 'rrover', 'rrunder', 'rsi_3', 'rsi_4', 'rsi_5',

'rsi_6', 'rsi_8', 'rsi_10', 'rsi_14', 'sep_3_3', 'sep_5_5', 'sep_8_8',

'sep_10_10', 'sep_14_14', 'sep_21_21', 'sep_30_30', 'sep_40_40',

'sephigh', 'seplow', 'trend', 'vma', 'vmover', 'vmratio', 'vmunder',

'volatility_3', 'volatility_5', 'volatility', 'volatility_20',

'wr_2', 'wr_3', 'wr', 'wr_5', 'wr_6', 'wr_7', 'wr_10']

aliases:

atr : 'ma_truerange'

aver : 'ma_hlrange'

cma : 'ma_close'

cmax : 'highest_close'

cmin : 'lowest_close'

hc : 'higher_close'

hh : 'higher_high'

hl : 'higher_low'

ho : 'higher_open'

hmax : 'highest_high'

hmin : 'lowest_high'

lc : 'lower_close'

lh : 'lower_high'

ll : 'lower_low'

lo : 'lower_open'

lmax : 'highest_low'

lmin : 'lowest_low'

net : 'net_close'

netdown : 'down_net'

netup : 'up_net'

omax : 'highest_open'

omin : 'lowest_open'

rmax : 'highest_hlrange'

rmin : 'lowest_hlrange'

rr : 'maratio_hlrange'

rixc : 'rindex_close_high_low'

rixo : 'rindex_open_high_low'

roi : 'netreturn_close'

rsi : 'rsi_close'

sepma : 'ma_sep'

vma : 'ma_volume'

vmratio : 'maratio_volume'

upmove : 'net_high'

variables:

abovema : 'close > cma_50'

belowma : 'close < cma_50'

bigup : 'rrover & sephigh & netup'

bigdown : 'rrover & sephigh & netdown'

doji : 'sepdoji & rrunder'

hookdown : 'open > high[1] & close < close[1]'

hookup : 'open < low[1] & close > close[1]'

inside : 'low > low[1] & high < high[1]'

madelta : '(close - cma_50) / atr_10'

nr : 'hlrange == rmin_4'

outside : 'low < low[1] & high > high[1]'

roihigh : 'roi_5 >= 5'

roilow : 'roi_5 < -5'

roiminus : 'roi_5 < 0'

roiplus : 'roi_5 > 0'

rrhigh : 'rr_1_10 >= 1.2'

rrlow : 'rr_1_10 <= 0.8'

rrover : 'rr_1_10 >= 1.0'

rrunder : 'rr_1_10 < 1.0'

sep : 'rixc_1 - rixo_1'

sepdoji : 'abs(sep) <= 15'

sephigh : 'abs(sep_1_1) >= 70'

seplow : 'abs(sep_1_1) <= 30'

trend : 'rrover & sephigh'

vmover : 'vmratio >= 1'

vmunder : 'vmratio < 1'

volatility : 'atr_10 / close'

wr : 'hlrange == rmax_4'

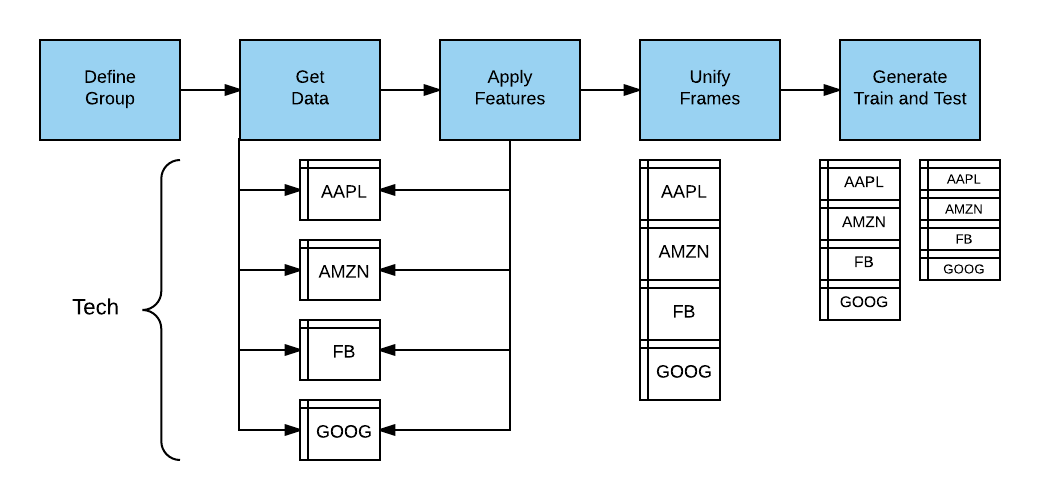

Group Analysis¶

The cornerstone of MarketFlow is the Analysis. You can create models and forecasts for different groups of stocks. The purpose of the analysis object is to gather data for all of the group members and then consolidate the data into train and test files. Further, some features and the target variable have to be adjusted (lagged) to avoid data leakage.

A group is simply a collection of symbols for analysis. In this

example, we create different groups for technology stocks, ETFs,

and a smaller group for testing. To create a model for a given

group, simply set the target_group in the market section

of the market.yml file and run mflow.

groups:

all : ['aaoi', 'aapl', 'acia', 'adbe', 'adi', 'adp', 'agn', 'aig', 'akam',

'algn', 'alk', 'alxn', 'amat', 'amba', 'amd', 'amgn', 'amt', 'amzn',

'antm', 'arch', 'asml', 'athn', 'atvi', 'auph', 'avgo', 'axp', 'ayx',

'azo', 'ba', 'baba', 'bac', 'bby', 'bidu', 'biib', 'brcd', 'bvsn',

'bwld', 'c', 'cacc', 'cara', 'casy', 'cat', 'cde', 'celg', 'cern',

'chkp', 'chtr', 'clvs', 'cme', 'cmg', 'cof', 'cohr', 'comm', 'cost',

'cpk', 'crm', 'crus', 'csco', 'ctsh', 'ctxs', 'csx', 'cvs', 'cybr',

'data', 'ddd', 'deck', 'dgaz', 'dia', 'dis', 'dish', 'dnkn', 'dpz',

'drys', 'dust', 'ea', 'ebay', 'edc', 'edz', 'eem', 'elli', 'eog',

'esrx', 'etrm', 'ewh', 'ewt', 'expe', 'fang', 'fas', 'faz', 'fb',

'fcx', 'fdx', 'ffiv', 'fit', 'five', 'fnsr', 'fslr', 'ftnt', 'gddy',

'gdx', 'gdxj', 'ge', 'gild', 'gld', 'glw', 'gm', 'googl', 'gpro',

'grub', 'gs', 'gwph', 'hal', 'has', 'hd', 'hdp', 'hlf', 'hog', 'hum',

'ibb', 'ibm', 'ice', 'idxx', 'ilmn', 'ilmn', 'incy', 'intc', 'intu',

'ip', 'isrg', 'iwm', 'ivv', 'iwf', 'iwm', 'jack', 'jcp', 'jdst', 'jnj',

'jnpr', 'jnug', 'jpm', 'kite', 'klac', 'ko', 'kss', 'labd', 'labu',

'len', 'lite', 'lmt', 'lnkd', 'lrcx', 'lulu', 'lvs', 'mbly', 'mcd',

'mchp', 'mdy', 'meoh', 'mnst', 'mo', 'momo', 'mon', 'mrk', 'ms', 'msft',

'mtb', 'mu', 'nflx', 'nfx', 'nke', 'ntap', 'ntes', 'ntnx', 'nugt',

'nvda', 'nxpi', 'nxst', 'oii', 'oled', 'orcl', 'orly', 'p', 'panw',

'pcln', 'pg', 'pm', 'pnra', 'prgo', 'pxd', 'pypl', 'qcom', 'qqq',

'qrvo', 'rht', 'sam', 'sbux', 'sds', 'sgen', 'shld', 'shop', 'sig',

'sina', 'siri', 'skx', 'slb', 'slv', 'smh', 'snap', 'sncr', 'soda',

'splk', 'spy', 'stld', 'stmp', 'stx', 'svxy', 'swks', 'symc', 't',

'tbt', 'teva', 'tgt', 'tho', 'tlt', 'tmo', 'tna', 'tqqq', 'trip',

'tsla', 'ttwo', 'tvix', 'twlo', 'twtr', 'tza', 'uaa', 'ugaz', 'uhs',

'ulta', 'ulti', 'unh', 'unp', 'upro', 'uri', 'ups', 'uri', 'uthr',

'utx', 'uvxy', 'v', 'veev', 'viav', 'vlo', 'vmc', 'vrsn', 'vrtx', 'vrx',

'vwo', 'vxx', 'vz', 'wday', 'wdc', 'wfc', 'wfm', 'wmt', 'wynn', 'x',

'xbi', 'xhb', 'xiv', 'xle', 'xlf', 'xlk', 'xlnx', 'xom', 'xlp', 'xlu',

'xlv', 'xme', 'xom', 'wix', 'yelp', 'z']

etf : ['dia', 'dust', 'edc', 'edz', 'eem', 'ewh', 'ewt', 'fas', 'faz',

'gld', 'hyg', 'iwm', 'ivv', 'iwf', 'jnk', 'mdy', 'nugt', 'qqq',

'sds', 'smh', 'spy', 'tbt', 'tlt', 'tna', 'tvix', 'tza', 'upro',

'uvxy', 'vwo', 'vxx', 'xhb', 'xiv', 'xle', 'xlf', 'xlk', 'xlp',

'xlu', 'xlv', 'xme']

tech : ['aapl', 'adbe', 'amat', 'amgn', 'amzn', 'avgo', 'baba', 'bidu',

'brcd', 'csco', 'ddd', 'emc', 'expe', 'fb', 'fit', 'fslr', 'goog',

'intc', 'isrg', 'lnkd', 'msft', 'nflx', 'nvda', 'pcln', 'qcom',

'qqq', 'tsla', 'twtr']

test : ['aapl', 'amzn', 'goog', 'fb', 'nvda', 'tsla']

Variables and Aliases¶

Because market analysis encompasses a wide array of technical indicators, you can define features using the Variable Definition Language (VDL). The concept is simple: flatten out a function call and its parameters into a string, and that string represents the variable name. You can use the technical analysis functions in AlphaPy, or define your own.

Let’s define a feature that indicates whether or not a stock is above

its 50-day closing moving average. The alphapy.market_variables

module has a function ma to calculate a rolling mean. It has two

parameters: the name of the dataframe’s column and the period over

which to calculate the mean. So, the corresponding variable name is

ma_close_50.

Typically, a moving average is calculated with the closing price,

so we can define an alias cma which represents the closing

moving average. An alias is simply a substitution mechanism for

replacing one string with an abbreviation. Instead of ma_close_50,

we can now refer to cma_50 using an alias.

Finally, we can define the variable abovema with a relational

expression. Note that numeric values in the expression can be

substituted when defining features, e.g., abovema_20.

features: ['abovema_50']

aliases:

cma : 'ma_close'

variables:

abovema : 'close > cma_50'

Here are more examples of aliases.

aliases:

atr : 'ma_truerange'

aver : 'ma_hlrange'

cma : 'ma_close'

cmax : 'highest_close'

cmin : 'lowest_close'

hc : 'higher_close'

hh : 'higher_high'

hl : 'higher_low'

ho : 'higher_open'

hmax : 'highest_high'

hmin : 'lowest_high'

lc : 'lower_close'

lh : 'lower_high'

ll : 'lower_low'

lo : 'lower_open'

lmax : 'highest_low'

lmin : 'lowest_low'

net : 'net_close'

netdown : 'down_net'

netup : 'up_net'

omax : 'highest_open'

omin : 'lowest_open'

rmax : 'highest_hlrange'

rmin : 'lowest_hlrange'

rr : 'maratio_hlrange'

rixc : 'rindex_close_high_low'

rixo : 'rindex_open_high_low'

roi : 'netreturn_close'

rsi : 'rsi_close'

sepma : 'ma_sep'

vma : 'ma_volume'

vmratio : 'maratio_volume'

upmove : 'net_high'

Variable expressions are valid Python expressions, with the addition of offsets to reference previous values.

variables:

abovema : 'close > cma_50'

belowma : 'close < cma_50'

bigup : 'rrover & sephigh & netup'

bigdown : 'rrover & sephigh & netdown'

doji : 'sepdoji & rrunder'

hookdown : 'open > high[1] & close < close[1]'

hookup : 'open < low[1] & close > close[1]'

inside : 'low > low[1] & high < high[1]'

madelta : '(close - cma_50) / atr_10'

nr : 'hlrange == rmin_4'

outside : 'low < low[1] & high > high[1]'

roihigh : 'roi_5 >= 5'

roilow : 'roi_5 < -5'

roiminus : 'roi_5 < 0'

roiplus : 'roi_5 > 0'

rrhigh : 'rr_1_10 >= 1.2'

rrlow : 'rr_1_10 <= 0.8'

rrover : 'rr_1_10 >= 1.0'

rrunder : 'rr_1_10 < 1.0'

sep : 'rixc_1 - rixo_1'

sepdoji : 'abs(sep) <= 15'

sephigh : 'abs(sep_1_1) >= 70'

seplow : 'abs(sep_1_1) <= 30'

trend : 'rrover & sephigh'

vmover : 'vmratio >= 1'

vmunder : 'vmratio < 1'

volatility : 'atr_10 / close'

wr : 'hlrange == rmax_4'

Once the aliases and variables are defined, a foundation is established for defining all of the features that you want to test.

features: ['abovema_3', 'abovema_5', 'abovema_10', 'abovema_20', 'abovema_50',

'adx', 'atr', 'bigdown', 'bigup', 'diminus', 'diplus', 'doji',

'gap', 'gapbadown', 'gapbaup', 'gapdown', 'gapup',

'hc', 'hh', 'ho', 'hl', 'lc', 'lh', 'll', 'lo', 'hookdown', 'hookup',

'inside', 'outside', 'madelta_3', 'madelta_5', 'madelta_7', 'madelta_10',

'madelta_12', 'madelta_15', 'madelta_18', 'madelta_20', 'madelta',

'net', 'netdown', 'netup', 'nr_3', 'nr_4', 'nr_5', 'nr_7', 'nr_8',

'nr_10', 'nr_18', 'roi', 'roi_2', 'roi_3', 'roi_4', 'roi_5', 'roi_10',

'roi_20', 'rr_1_4', 'rr_1_7', 'rr_1_10', 'rr_2_5', 'rr_2_7', 'rr_2_10',

'rr_3_8', 'rr_3_14', 'rr_4_10', 'rr_4_20', 'rr_5_10', 'rr_5_20',

'rr_5_30', 'rr_6_14', 'rr_6_25', 'rr_7_14', 'rr_7_35', 'rr_8_22',

'rrhigh', 'rrlow', 'rrover', 'rrunder', 'rsi_3', 'rsi_4', 'rsi_5',

'rsi_6', 'rsi_8', 'rsi_10', 'rsi_14', 'sep_3_3', 'sep_5_5', 'sep_8_8',

'sep_10_10', 'sep_14_14', 'sep_21_21', 'sep_30_30', 'sep_40_40',

'sephigh', 'seplow', 'trend', 'vma', 'vmover', 'vmratio', 'vmunder',

'volatility_3', 'volatility_5', 'volatility', 'volatility_20',

'wr_2', 'wr_3', 'wr', 'wr_5', 'wr_6', 'wr_7', 'wr_10']

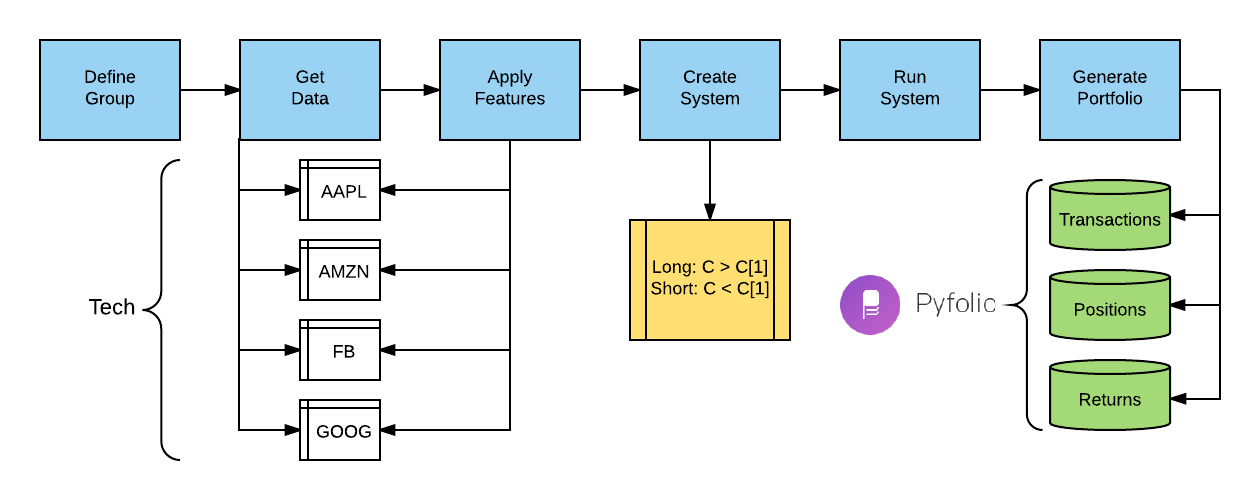

Trading Systems¶

MarketFlow provides two out-of-the-box trading systems. The first is

a long/short system that you define using the system features in the

configuration file market.yml. When MarketFlow detects a system

in the file, it knows to execute that particular long/short strategy.

market:

data_history : 1000

forecast_period : 1

fractal : 1d

leaders : []

predict_history : 50

schema : prices

target_group : faang

system:

name : 'closer'

holdperiod : 0

longentry : hc

longexit :

shortentry : lc

shortexit :

scale : False

groups:

faang : ['fb', 'aapl', 'amzn', 'nflx', 'googl']

features : ['hc', 'lc']

aliases:

hc : 'higher_close'

lc : 'lower_close'

name:Unique identifier for the trading system.

holdperiod:Number of periods to hold an open position.

longentry:A conditional feature to establish when to open a long position.

longexit:A conditional feature to establish when to close a long position.

shortentry:A conditional feature to establish when to open a short position.

shortexit:A conditional feature to establish when to close a short position.

scale:When

True, add to a position in the same direction. The default action is not to scale positions.

The second system is an open range breakout strategy. The premise of the system is to wait for an established high-low range in the first n minutes (e.g., 30) and then wait for a breakout of either the high or the low, especially when the range is relatively narrow. Typically, a stop-loss is set at the other side of the breakout range.

After a system runs, four output files are stored in the system

directory; the first three are formatted for analysis by Quantopian’s

pyfolio package. The last file is the list of trades generated

by MarketFlow based on the system specifications.

[group]_[system]_transactions_[fractal].csv

[group]_[system]_positions_[fractal].csv

[group]_[system]_returns_[fractal].csv

[group]_[system]_trades_[fractal].csv

If we developed a moving average crossover system on daily data for technology stocks, then the trades file could be named:

tech_xma_trades_1d.csv

The important point here is to reserve a namespace for different combinations of groups, systems, and fractals to compare performance over space and time.

Model Configuration¶

MarketFlow runs on top of AlphaPy, so the model.yml file has

the same format. In the following example, note the use of treatments

to calculate runs for a set of features.

project:

directory : .

file_extension : csv

submission_file :

submit_probas : False

data:

drop : ['date', 'tag', 'open', 'high', 'low', 'close', 'volume', 'adjclose',

'low[1]', 'high[1]', 'net', 'close[1]', 'rmin_3', 'rmin_4', 'rmin_5',

'rmin_7', 'rmin_8', 'rmin_10', 'rmin_18', 'pval', 'mval', 'vma',

'rmax_2', 'rmax_3', 'rmax_4', 'rmax_5', 'rmax_6', 'rmax_7', 'rmax_10']

features : '*'

sampling :

option : True

method : under_random

ratio : 0.5

sentinel : -1

separator : ','

shuffle : True

split : 0.4

target : rrover

target_value : True

model:

algorithms : ['RF']

balance_classes : True

calibration :

option : False

type : isotonic

cv_folds : 3

estimators : 501

feature_selection :

option : True

percentage : 50

uni_grid : [5, 10, 15, 20, 25]

score_func : f_classif

grid_search :

option : False

iterations : 100

random : True

subsample : True

sampling_pct : 0.25

pvalue_level : 0.01

rfe :

option : True

step : 10

scoring_function : 'roc_auc'

type : classification

features:

clustering :

option : False

increment : 3

maximum : 30

minimum : 3

counts :

option : False

encoding :

rounding : 3

type : factorize

factors : []

interactions :

option : True

poly_degree : 2

sampling_pct : 5

isomap :

option : False

components : 2

neighbors : 5

logtransform :

option : False

numpy :

option : False

pca :

option : False

increment : 3

maximum : 15

minimum : 3

whiten : False

scaling :

option : True

type : standard

scipy :

option : False

text :

ngrams : 1

vectorize : False

tsne :

option : False

components : 2

learning_rate : 1000.0

perplexity : 30.0

variance :

option : True

threshold : 0.1

treatments:

doji : ['alphapy.features', 'runs_test', ['all'], 18]

hc : ['alphapy.features', 'runs_test', ['all'], 18]

hh : ['alphapy.features', 'runs_test', ['all'], 18]

hl : ['alphapy.features', 'runs_test', ['all'], 18]

ho : ['alphapy.features', 'runs_test', ['all'], 18]

rrhigh : ['alphapy.features', 'runs_test', ['all'], 18]

rrlow : ['alphapy.features', 'runs_test', ['all'], 18]

rrover : ['alphapy.features', 'runs_test', ['all'], 18]

rrunder : ['alphapy.features', 'runs_test', ['all'], 18]

sephigh : ['alphapy.features', 'runs_test', ['all'], 18]

seplow : ['alphapy.features', 'runs_test', ['all'], 18]

trend : ['alphapy.features', 'runs_test', ['all'], 18]

pipeline:

number_jobs : -1

seed : 10231

verbosity : 0

plots:

calibration : True

confusion_matrix : True

importances : True

learning_curve : True

roc_curve : True

xgboost:

stopping_rounds : 20

Creating the Model¶

First, change the directory to your project location, where you have already followed the Project Structure specifications:

cd path/to/project

Run this command to train a model:

mflow

Usage:

mflow [--train | --predict] [--tdate yyyy-mm-dd] [--pdate yyyy-mm-dd]

- --train

Train a new model and make predictions (Default)

- --predict

Make predictions from a saved model

- --tdate

The training date in format YYYY-MM-DD (Default: Earliest Date in the Data)

- --pdate

The prediction date in format YYYY-MM-DD (Default: Today’s Date)

Running the Model¶

In the project location, run mflow with the predict flag.

MarketFlow will automatically create the predict.csv file using

the pdate option:

mflow --predict [--pdate yyyy-mm-dd]